Affordability of Property Prices in terms of Household Income

Concept

The following analysis method will evaluate property prices by examining their affordability for different income classes. It seeks to establish whether there are sufficient acceptable property purchase options for all the various income classes in the different areas of Cape Town. It is suggested that a sufficient amount of appropriate property purchase options for different levels of household income must be available. A lack of appropriate property purchase options suggests that housing prices are overvalued.

Method

Due to outdated sources for average annual income of households (the latest statistical release of income and expenditure in South Africa was for the years 2005/2006), as well as skewed data of other salary surveys it was difficult to establish a real average salary per annum for households in Cape Town. Therefore the affordability of property prices will be established by means of five different benchmark salaries. Unfortunately, the property sales and price data relevant to low cost housing is not available, and consequently the affordability of property by the many people closer to the poverty line has not been considered in this report.

For each of the five household income benchmarks a bond limit is calculated based on the following criteria:

-The loan repayment may not exceed 30% of the household’s gross income.

-The interest rate is 9%

-The loan is granted for 100% of the purchase price of the property.

-The loan is repaid over a 20 year duration.

By means of the average property prices of 2011 the purchasing power for each of the household income benchmarks will be established. The purchasing power is expressed in square meters, indicating the size of dwelling a specific household can afford to purchase in each area.

Analysis

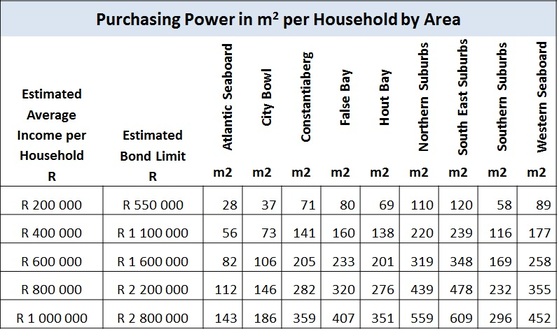

The table below shows the different household income benchmarks from R 200 000 per annum up to R 1 000 000 per annum. Bond limits were established according to the 30% gross income rule. The table shows the different unit sizes in different areas that are affordable by the different household benchmarks.

The following analysis method will evaluate property prices by examining their affordability for different income classes. It seeks to establish whether there are sufficient acceptable property purchase options for all the various income classes in the different areas of Cape Town. It is suggested that a sufficient amount of appropriate property purchase options for different levels of household income must be available. A lack of appropriate property purchase options suggests that housing prices are overvalued.

Method

Due to outdated sources for average annual income of households (the latest statistical release of income and expenditure in South Africa was for the years 2005/2006), as well as skewed data of other salary surveys it was difficult to establish a real average salary per annum for households in Cape Town. Therefore the affordability of property prices will be established by means of five different benchmark salaries. Unfortunately, the property sales and price data relevant to low cost housing is not available, and consequently the affordability of property by the many people closer to the poverty line has not been considered in this report.

For each of the five household income benchmarks a bond limit is calculated based on the following criteria:

-The loan repayment may not exceed 30% of the household’s gross income.

-The interest rate is 9%

-The loan is granted for 100% of the purchase price of the property.

-The loan is repaid over a 20 year duration.

By means of the average property prices of 2011 the purchasing power for each of the household income benchmarks will be established. The purchasing power is expressed in square meters, indicating the size of dwelling a specific household can afford to purchase in each area.

Analysis

The table below shows the different household income benchmarks from R 200 000 per annum up to R 1 000 000 per annum. Bond limits were established according to the 30% gross income rule. The table shows the different unit sizes in different areas that are affordable by the different household benchmarks.

It should be noted that all households have purchase options of reasonably sized property in all areas of Cape Town, with the exception of the first household benchmark of R 200 000, which has limited purchasing power in areas such as the Atlantic Seaboard, and possibly the City Bowl, as well as the Southern Suburbs.

Looking at the first salary scale of R200 000 in more detail, one could assume that a household with this income might consist of a young couple where both parties are in an office administration role. As mentioned above, the purchasing power for this income bracket in the Atlantic Seaboard is limited and it is unlikely that the couple would be able to afford a reasonably sized property. However, there are plenty of options in all the other areas listed above. Even if the couple is planning to start a family in the near future they are still able to purchase a property large enough to cater for a family in the Northern Suburbs or South East Suburbs.

This household (R 200 000 benchmark) could also consist of a single young professional with a few years working experience. In this case, the more expensive suburbs such as Southern Suburbs, City Bowl, and possibly the Atlantic Seaboard become a more viable option, as a single person will require less space than a couple.

Considering a higher income benchmark such as R600 000 for example, it can be noticed that purchasing options increase and even property in the Atlantic Seaboard presents itself as a viable choice. A young couple, possibly a professional with a number of years’ experience and his or her partner being a start-up entrepreneur, could choose between a decent sized apartment in the Atlantic Seaboard, possibly with sea view if they settle for a smaller sized property, or a larger property, possibly with garden in False Bay, Hout Bay, Southern Suburbs or the Western Seaboard. The Northern Suburbs provide even larger property purchase options. In theory, such a couple could settle anywhere in Cape Town depending on their needs in terms of travelling to work, property size and future family plans.

The purchasing power for the various income levels in the different areas is illustrated in the chart below

Looking at the first salary scale of R200 000 in more detail, one could assume that a household with this income might consist of a young couple where both parties are in an office administration role. As mentioned above, the purchasing power for this income bracket in the Atlantic Seaboard is limited and it is unlikely that the couple would be able to afford a reasonably sized property. However, there are plenty of options in all the other areas listed above. Even if the couple is planning to start a family in the near future they are still able to purchase a property large enough to cater for a family in the Northern Suburbs or South East Suburbs.

This household (R 200 000 benchmark) could also consist of a single young professional with a few years working experience. In this case, the more expensive suburbs such as Southern Suburbs, City Bowl, and possibly the Atlantic Seaboard become a more viable option, as a single person will require less space than a couple.

Considering a higher income benchmark such as R600 000 for example, it can be noticed that purchasing options increase and even property in the Atlantic Seaboard presents itself as a viable choice. A young couple, possibly a professional with a number of years’ experience and his or her partner being a start-up entrepreneur, could choose between a decent sized apartment in the Atlantic Seaboard, possibly with sea view if they settle for a smaller sized property, or a larger property, possibly with garden in False Bay, Hout Bay, Southern Suburbs or the Western Seaboard. The Northern Suburbs provide even larger property purchase options. In theory, such a couple could settle anywhere in Cape Town depending on their needs in terms of travelling to work, property size and future family plans.

The purchasing power for the various income levels in the different areas is illustrated in the chart below

It is needless to say that the purchasing power gets stronger with increasing income. But is the property purchasing power as strong as one would want it to be when forming part of the income benchmark of R1 000 000? A senior manager with approximately two decades experience should be able to earn a gross income of approximately R1 000 000. He supports his wife, a full time mother, and his two children. Based on 2012/2013 income tax figures, he would earn a net salary of approximately R56 000 per month excluding medical aid and pension fund deductions. After these deductions the take-home salary would be in the region of R45 000 per month; deducting the bond repayment (for the estimated bond limit as stated in Table 8 of R2 800 000) of approximately R25 000 per month will leave the family with R20 000 per month to survive. Once school fees and various insurance premiums are taken into account, the remainder left would be approximately R10 000 per month which should be sufficient to cover general household expenses for a family of four.

If the family’s monthly budget exceeds R10 000 per month the household could choose to buy in a more affordable area or a smaller-sized property to reduce the monthly mortgage payments. In addition, it is unlikely that the household is a first-time purchaser and would most likely be in possession of a property which was previously bought. The household could sell their current property in order to finance the upgrade of their family home.

The analysis and evaluation of purchasing power of different household incomes in terms of dwelling size and area has shown that there are sufficient purchasing options for all of the various income benchmarks selected. This would suggest that housing prices are correctly priced, with possibly the exception of the Atlantic Seaboard and the City Bowl areas, as the purchasing power for all income levels in these areas are substantially lower than in other areas. The strong purchasing power in areas such as Northern Suburbs and South East Suburbs even for low income levels suggest a possible under-pricing or alternatively over-pricing in other areas.

If the family’s monthly budget exceeds R10 000 per month the household could choose to buy in a more affordable area or a smaller-sized property to reduce the monthly mortgage payments. In addition, it is unlikely that the household is a first-time purchaser and would most likely be in possession of a property which was previously bought. The household could sell their current property in order to finance the upgrade of their family home.

The analysis and evaluation of purchasing power of different household incomes in terms of dwelling size and area has shown that there are sufficient purchasing options for all of the various income benchmarks selected. This would suggest that housing prices are correctly priced, with possibly the exception of the Atlantic Seaboard and the City Bowl areas, as the purchasing power for all income levels in these areas are substantially lower than in other areas. The strong purchasing power in areas such as Northern Suburbs and South East Suburbs even for low income levels suggest a possible under-pricing or alternatively over-pricing in other areas.